Can you live without 44% of your current income? Are you relying solely on your State Teachers’ Pension Plan?

While your State Teachers’ Pension Plan will provide a valuable source of ongoing retirement income, your pension probably won’t provide enough income to ensure a financially secure retirement. In fact, the statistic on some of the State Teachers’ Pension Plan websites show a loss of approximately 44% of your income, in retirement. Want security? One way to save for retirement is in a 403(b) plan. It’s never too early to start investing in your future.

Let’s look at some numbers:

- 40% – 44% = The percentage an employee’s income will decrease during retirement.¹

- 70% – 90% = The percentage of your current income needed to maintain a comfortable lifestyle in retirement.²

- 50% = The percentage of employees who feel more confident about having enough money to live comfortably throughout retirement because they have participated in a retirement plan other than their pension.³

- 0% = The percentage of income most school employees will receive from Social Security.⁴

As you can see, there is a gap between the amount of income provided by the average State Teachers’ Pension Plan and the amount of income you will likely need to live a comfortable lifestyle in retirement. To increase the income available to you in retirement, you’ll need to supplement your State Teachers’ Pension Plan with your own personal retirement plan.

¹Information obtained from Texas TRS and California CalSTRS.

²Information obtained from Texas TRS and California CalSTRS.

³Information obtained from Employee Benefit Research Institute.

⁴Information obtained from Texas TRS, CalSTRS, and Social Security.

HOW CAN A 403(B) WORK FOR YOU?

With a 403(b) plan, contributions are deducted from your paycheck on a pre-tax basis. Taxes on your 403(b) contributions are deferred until you begin making withdrawals, which typically happens at retirement. This offers several tax advantages:

CONTRIBUTIONS ARE

CONTRIBUTIONS ARE

TAX DEDUCTIBLE

The actual reduction to your take-home pay will be less than your contribution amount. To provide a simplified example, let’s say you’re in the 25% tax bracket. A $100 pre-tax contribution to your 403(b) plan may reduce your take-home pay by an additional $75, since that $100 would have been taxed 25% if you had not deferred it into your 403(b) plan.⁵

⁵Source IRS website

SAVINGS GROW

TAX FREE

The earnings and gains on your 403(b) plan will grow tax-free until withdrawal. All earnings and gains will remain in your 403(b) to potentially earn more. Although you will eventually have to pay taxes when you withdraw your money, you will likely benefit from years of compounding interest on your untaxed earnings.⁶

A huge advantage of a 403(b) plan is that you do not have to pay taxes on earnings and/or gains held in your 403(b) plan.

⁶Source IRS website

CONTRIBUTION LIMITS

ARE HIGHER THAN

AN IRA ACCOUNT

The more money that you can save for your retirement on a tax-sheltered basis, the better off you will be. As an employee, you can put up to $18,500 into a 403(b) plan as of 2018. Employees who are age 50 or older may be eligible to make up to a $6,000 additional “catch up” contribution as of 2018. These contribution limits are huge compared with the $5,500 limit and $1,000 catch up limits on IRAs.⁷

⁷Source IRS website

WAITING MAY COST YOU, SO GET STARTED TODAY

When it comes to retirement planning, it’s never too early to start saving. The more you save and the earlier you start means your 403(b) plan will have much more time and potential to grow. By investing early, you will be able to take advantage of compound earnings.

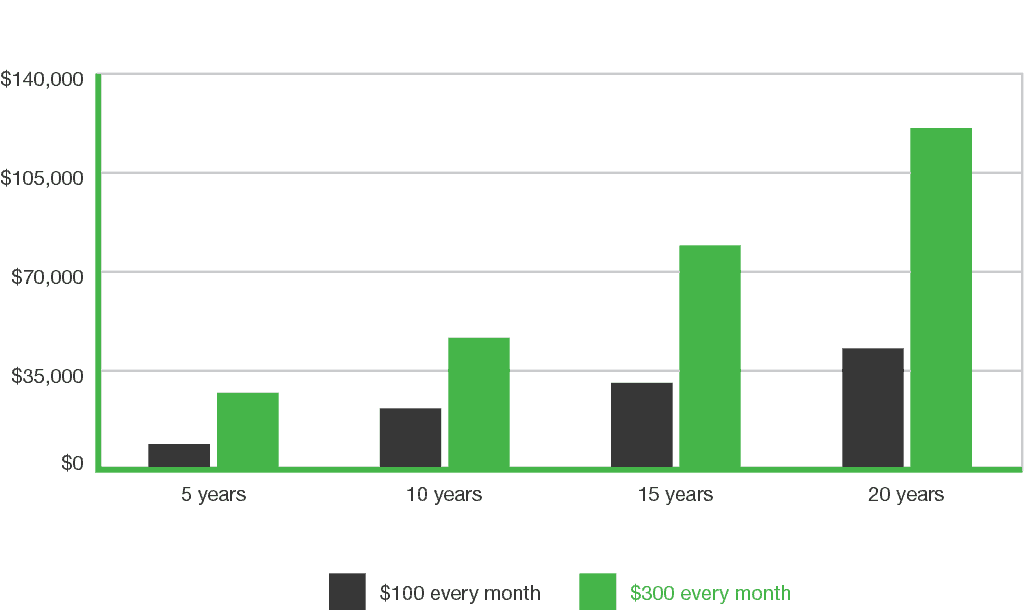

Let’s say you contribute $100 a month to your 403(b) plan directly from your paycheck. If your 403(b) plan averages a 5 percent rate of return annually, after 20 years you could have $41,103. If you increase your monthly contribution to $300 a month, your savings could grow to $123,310. An added benefit of tax-deferred contributions: Your $300 investment may reduce your paycheck by only $225 based on a 25% tax savings.

A LITTLE NOW CAN REALLY ADD UP LATER

GIVE US A CALL

214-295-2788

OUR HOURS

Monday-Friday

8AM – 5PM

E-MAIL US

VISIT OUR OFFICE

516 South Wheeler St

Jasper, TX – 75951